For many people, particularly business owners, cash feels like the safest place to keep money.

It’s visible.

It’s tangible.

It doesn’t go down in value on a statement.

That sense of control is reassuring. After all, if the number in the bank account hasn’t fallen, it feels like the money is safe.

But there’s a common myth hidden inside that thinking.

Cash may protect the number you see, but it doesn’t protect what that money can actually buy.

The Myth of Cash: How Inflation Quietly Erodes Purchasing Power

Inflation is the quiet force that erodes the real value of money over time.

Prices for goods, services, energy and travel gradually increase, meaning the same amount of money buys less as the years pass.

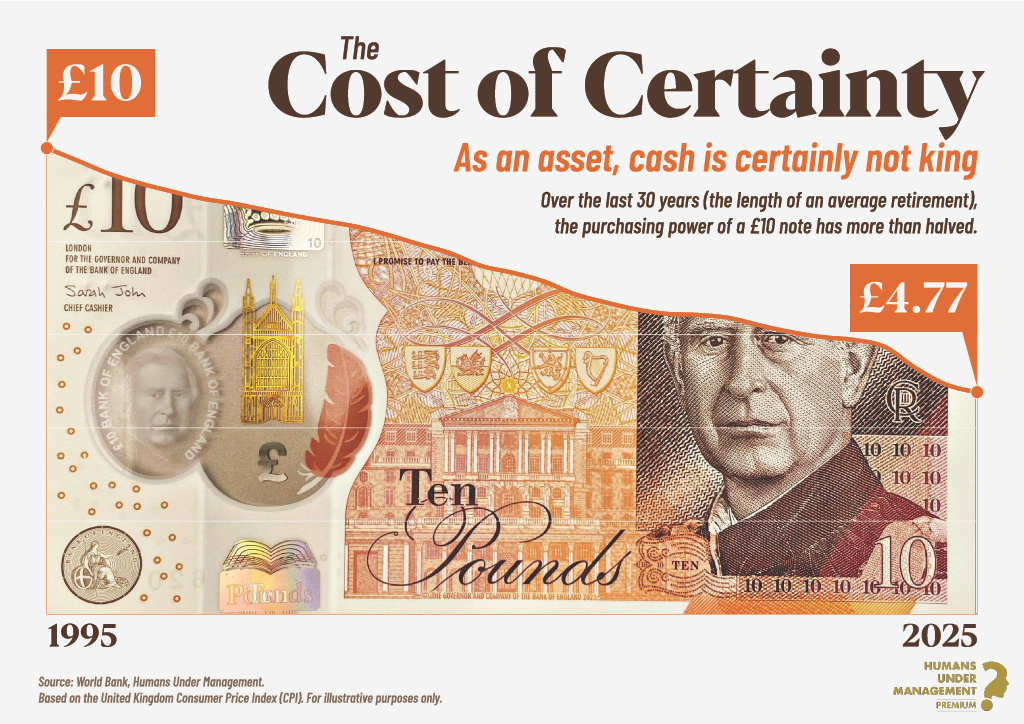

A simple illustration highlights the impact.

If you held £100,000 in cash in March 2021, today that same £100,000 would have the purchasing power of roughly £85,000.

The number hasn’t changed.

But what it can buy has.

This is the challenge with holding large amounts of cash for long periods. While it may feel secure because it doesn’t fluctuate, its real value is steadily declining.

For individuals and businesses alike, that’s an issue worth thinking about.

Cash Is Accessible, But It’s Not Productive

Cash has an important role.

It provides flexibility, security and immediate access when needed. For business owners especially, liquidity can mean opportunity.

But there is an important distinction between accessible money and productive money.

If cash is sitting idle and not being used or spent, it isn’t generating growth. It’s not working beyond its basic purpose as a store of value.

Over time, that means it’s failing to reach its full potential.

In simple terms:

If you’re not spending your cash, it isn’t making you any money.

A Different Outcome When Money Is Invested

Contrast that with a long-term investment approach.

For example, if £100,000 had been invested in a broadly diversified portfolio such as the Vanguard LifeStrategy 80% Equity Fund in March 2021, the value would have moved up and down with markets over the period.

That volatility can feel uncomfortable at times — especially compared with the stability of cash.

However, over that same timeframe the investment would still have grown overall and, importantly, increased its purchasing power after inflation.

This illustrates one of the key differences between saving and investing:

- Savings protect capital stability

- Investments aim to protect and grow real purchasing power

Neither replaces the other. They simply serve different roles.

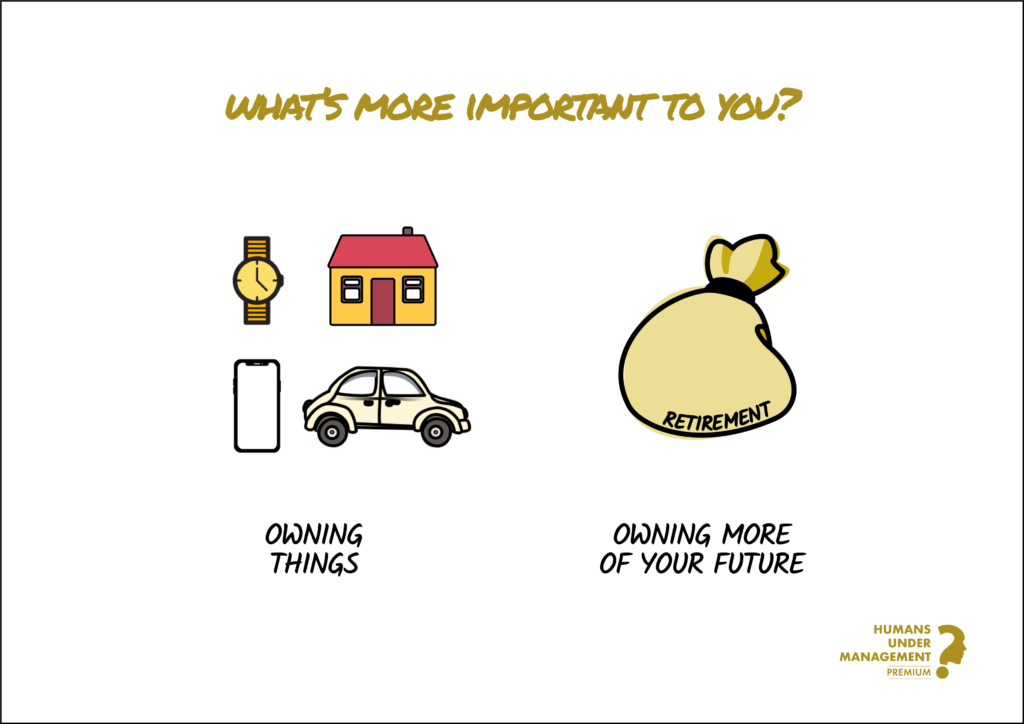

Two Pots: A Simpler Way to Think About It

One of the easiest ways to approach this is by separating money into two clear “pots”.

The Spending Pot

This is your accessible cash.

It’s there for:

- Emergencies

- Lifestyle spending

- Business liquidity

- The fun stuff — holidays, experiences and opportunities

Cash works perfectly here because the money may be needed quickly.

Booking a trip to the sun next summer?

Cash is ideal.

The Future Pot

This is where investing becomes important.

Money that isn’t needed for several years has time to grow and compound. Rather than gradually losing purchasing power to inflation, it has the opportunity to increase in real value.

This pot is designed for:

- Long-term wealth building

- Financial independence

- Future lifestyle plans

- The bucket-list experiences still ten or twenty years away

That dream trip around the world in a decade’s time?

Cash alone is unlikely to get you there.

Stability vs Progress

Cash is often described as “safe” because it doesn’t fluctuate.

But when inflation is taken into account, leaving large sums in cash indefinitely can actually introduce a different type of risk — the slow erosion of wealth.

The goal isn’t to abandon cash entirely.

It’s simply to recognise its purpose.

Cash provides stability and accessibility.

Investments provide growth and future purchasing power.

Used together, they create a more balanced financial strategy.

A Final Thought

The most financially confident individuals and businesses rarely choose between saving or investing.

They understand when each tool should be used.

Cash for today.

Investments for tomorrow.

Because the real question isn’t whether your money is safe sitting in the bank.

It’s whether it’s still working for you in ten years’ time.

If this article has prompted you to think differently about how your capital is structured, a conversation with the right adviser can provide clarity.

Our team works with individuals and business owners to help structure capital in a way that balances security today with growth for the future.

Speak to one of our advisers here: https://snfinancial.co.uk/about-us/

The value of your investment can fall as well as rise and is not guaranteed. You may not get back the full amount invested.